A few years ago, I was sitting on my living room couch, enjoying a quiet Friday evening, when I heard a sickening, rhythmic thump-thump-thump coming from the utility closet.

I opened the door to find my water heater staging a violent protest, leaking rusty water all over the floor.

At that exact moment, my bank account held a grand total of $142. My credit cards were already uncomfortably close to their limits from a recent vacation, and payday was a week away. The plumber’s estimate to replace the unit was $1,800.

I remember the exact mixture of panic, shame, and sheer helplessness that washed over me. I had to beg a family member for a loan, promise to pay them back with interest, and spend the next six months living on ramen and anxiety just to clear the debt.

That water heater disaster was my financial wake-up call. It was the moment I realized that living paycheck to paycheck wasn’t just stressful—it was a trap waiting to spring.

If you are currently staring at a tiny bank balance, wondering how on earth you’re supposed to save thousands of dollars when everything from groceries to gas feels impossibly expensive, I get it. But I also know you can break the cycle. I did it, and I’m going to show you exactly how to build an emergency fund from scratch, without losing your sanity or your lifestyle.

If you search for financial advice on Google, most "gurus" will tell you to immediately save three to six months' worth of living expenses.

Let's be completely honest: when you’re starting from zero, hearing that you need to save $15,000 feels like being told to climb Mount Everest in flip-flops. It’s so overwhelming that most people just give up before they even start.

When I decided to rebuild my finances, I threw that advice out the window.

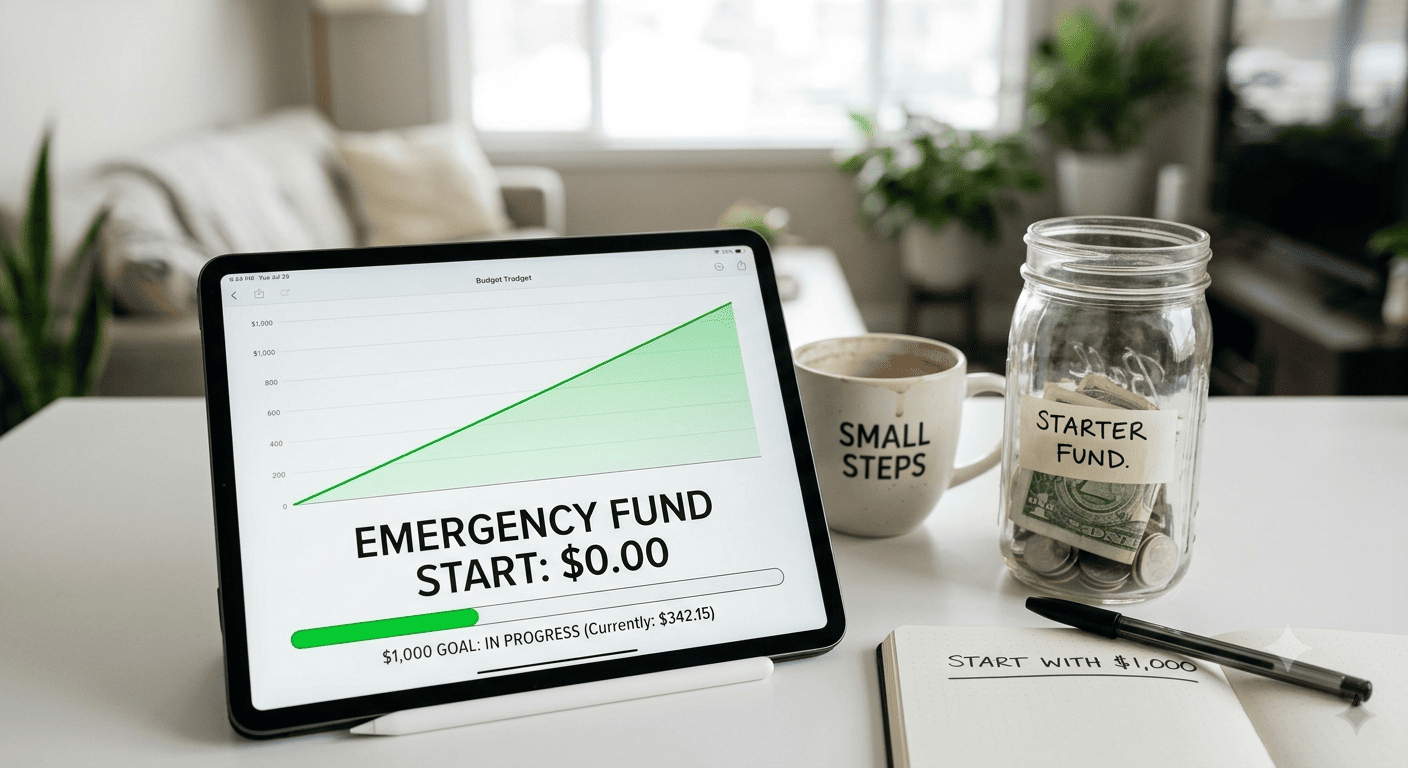

Instead, I focused on a much smaller, psychological milestone: The Starter Fund.

Your initial goal isn't to survive a six-month layoff; it’s to survive the next flat tire, broken phone screen, or dental bill. Your starter goal is exactly $1,000.

Once I shifted my focus from a massive, intimidating five-figure number to a manageable $1,000, something in my brain clicked. It stopped feeling like a punishment and started feeling like a game I could actually win.

Here is the exact framework I used to go from $0 to a fully funded emergency cushion. No complex spreadsheets required.

The biggest mistake I made initially was keeping my savings in the same bank as my checking account. Every time I logged into my mobile app, I saw that little pool of savings money sitting there, practically begging to be spent on a weekend trip or a flash sale.

To fix this, you need to practice out-of-sight, out-of-mind banking.

Open an account at an entirely different online bank. Look for a High-Yield Savings Account (HYSA). Online platforms like Ally Bank, Marcus by Goldman Sachs, or Wealthfront are great options. They don't charge monthly fees, and they pay significantly higher interest rates than traditional brick-and-mortar banks.

Once the account is open, do something radical: delete the bank's app from your phone. Make it just annoying enough to access that you won't touch it unless there is a genuine crisis.

If you wait until the end of the month to save "whatever is left over," you will never save a dime. There is never anything left over. Parkinson’s Law dictates that our spending will always expand to match our available income.

Instead, you have to trick yourself.

Set up an automated transfer on your payday for an amount so small you won't even notice it's gone. I started with just $25 a week.

Think about it: $25 is a couple of fancy coffee runs or a single takeout lunch. You won't miss it. But over the course of a year, that automated $25 a week turns into $1,300 without you ever having to make a conscious decision to save.

We are all bleeding money through micro-transactions we’ve completely forgotten about.

Sit down with your bank statements from the last 60 days. Look for recurring charges. That streaming service you haven’t watched in three months? Cancel it. The premium fitness app you used twice? Cancel it. The cloud storage upgrade you don’t need? Downgrade it.

When I did this, I uncovered $84 a month in zombie subscriptions. I didn't pocket that money; I immediately redirected that exact $84 into my new online savings account via auto-pay.

Whenever you get money that sits outside your normal paycheck, give it a job.

Tax refunds? Put 50% toward the fund.

Birthday cash from your grandmother? Put it in the fund.

Selling an old laptop or some clothes on Facebook Marketplace? Put it in the fund.

Windfalls are the ultimate accelerator. They turn a slow, steady climb into a massive leap forward.

Let's look at how this works in practice. Meet two scenarios based on people I've helped walk through this exact process.

Sarah makes $40,000 a year and feels like she has absolutely no breathing room. She can't afford to drop $100 a week into savings.

Her Strategy: Sarah signs up for a round-up app like Acorns or turns on the round-up feature in her banking app. Every time she buys something, the transaction rounds up to the nearest dollar, and the change goes to savings. She also cuts out ordering delivery apps (UberEats/DoorDash) for just one month.

The Result: Between the round-ups ($30/month) and cooking at home ($120/month), she finds $150 a month. In less than seven months, she hits her $1,000 starter goal.

Alex freelances and drives rideshare. His income fluctuates wildly every single week, making fixed automated transfers impossible.

His Strategy: Alex uses the "Percentage Rule." Every time a client pays him or a weekly deposit hits his account, he immediately transfers 5% of it to his HYSA. If it's a good week and he makes $1,000, he saves $50. If it's a slow week and he only makes $300, he saves $15.

The Result: Because the savings scale with his income, he never feels choked for cash during lean weeks, yet he still builds his safety net steadily over time.

Building an emergency fund isn't just about math; it's about behavior. Along the way, I made several slip-ups that set me back months.

About three months into my saving journey, a concert blew up my social media feed. All my friends were going. I looked at my growing savings account, convinced myself that "mental health emergencies count," and blew $300 on a ticket.

Guess what happened two weeks later? My car alternator died.

An emergency is not a vacation, a holiday gift, a flash sale, or a concert. An emergency is something that is unexpected, absolutely necessary, and urgent. If it doesn't fit all three criteria, keep your hands off the money.

You will likely have to dip into your emergency fund before it's fully built. That is completely normal.

I remember feeling incredibly defeated the first time I had to pull $200 out of my starter fund for a medical co-pay. I felt like a failure and wanted to give up on the whole project.

But then I realized: the fund did exactly what it was supposed to do. It kept me from putting that $200 on a high-interest credit card. Stepping back down to $500 isn't a failure; it's just part of the rhythm of life. You simply reset and start building again.

The day I finally crossed the $1,000 mark, nothing physically changed in my life. The apartment looked the same. My old car still rattled when I started it.

But mentally, everything shifted.

For the first time in my adult life, I didn't feel a pit in my stomach when I opened my mail. I stopped fearing my phone ringing with unknown numbers. I realized that an emergency fund isn't just a pile of cash; it's an insurance policy against anxiety. It buys you time, options, and sleep.

Once you hit that first $1,000, keep the momentum going. Gradually increase your automated transfers until you have three months of true living expenses tucked away.

Don't wait for your water heater to start leaking to take control of your financial story. Open that separate account today, set up a tiny automatic transfer, and give your future self the gift of breathing room. You've got this.

Posted on July 13th, 2026

Posted on July 12th, 2026

Posted on July 12th, 2026

Posted on July 10th, 2026

Posted on July 5th, 2026

Posted on July 1st, 2026

Posted on July 1st, 2026

Posted on June 27th, 2026

Posted on June 22nd, 2026

Posted on May 25th, 2026

Posted on May 1st, 2026

Posted on April 29th, 2026

Posted on April 20th, 2026

Posted on April 20th, 2026

Posted on April 18th, 2026

Posted on April 18th, 2026

Posted on April 14th, 2026

Posted on April 14th, 2026

Posted on March 30th, 2026

Posted on March 27th, 2026

Posted on March 27th, 2026

Posted on March 25th, 2026

Posted on March 23rd, 2026

Posted on February 3rd, 2026

Posted on January 16th, 2026

Posted on January 16th, 2026

Posted on January 16th, 2026

Posted on January 9th, 2026

Posted on October 27th, 2025

Posted on October 26th, 2025

Posted on August 7th, 2024

Posted on July 18th, 2024

Posted on July 17th, 2024

Posted on April 3rd, 2024

Posted on March 3rd, 2024

Posted on January 24th, 2024

Posted on January 11th, 2024

Posted on November 30th, 2023

Posted on November 10th, 2023

Posted on October 22nd, 2023

Posted on July 2nd, 2023

Posted on June 18th, 2023

Posted on June 12th, 2023

Posted on June 12th, 2023

Posted on June 11th, 2023

Posted on June 11th, 2023

2023 © SeenClassified All rights reserved.

Contact Us